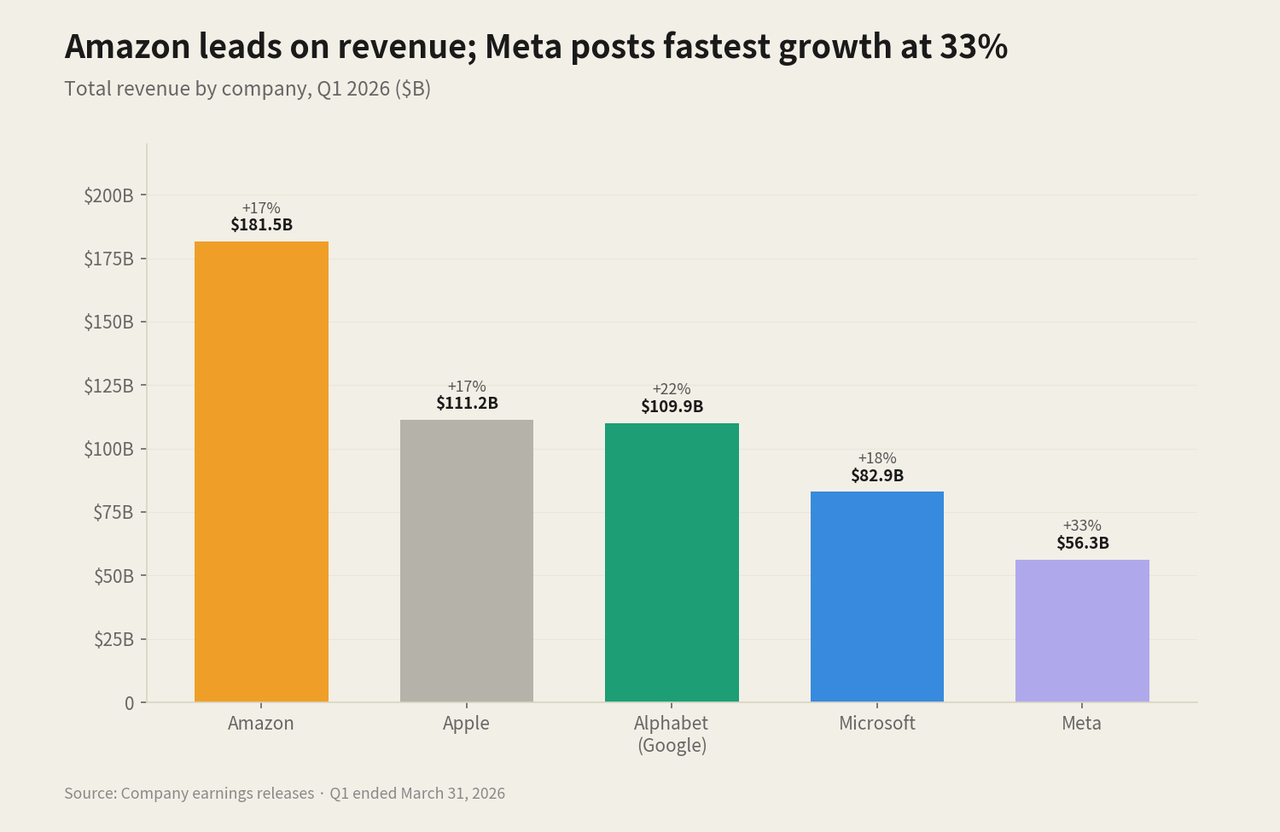

I. The Big Picture: $540B+ in Combined Revenue, AI the Unifying Theme

- Microsoft reported $82.9 billion in revenue, an 18% increase year over year.

- Alphabet posted $109.9 billion, up 22%, marking its 11th consecutive quarter of double-digit growth.

- Amazon achieved $181.5 billion, up 17%, with AWS revenue rising 28% to $37.6 billion, its fastest growth in 15 quarters.

- Meta's revenue reached $56.3 billion, a 33% increase and its fastest quarterly growth since 2021.

- Apple delivered its best-ever March quarter, reporting revenue of $111.2 billion, up 17%, with double-digit growth across all geographic segments and product categories.

II. Microsoft: AI Annual Revenue Run Rate Hits $37B, Up 123%

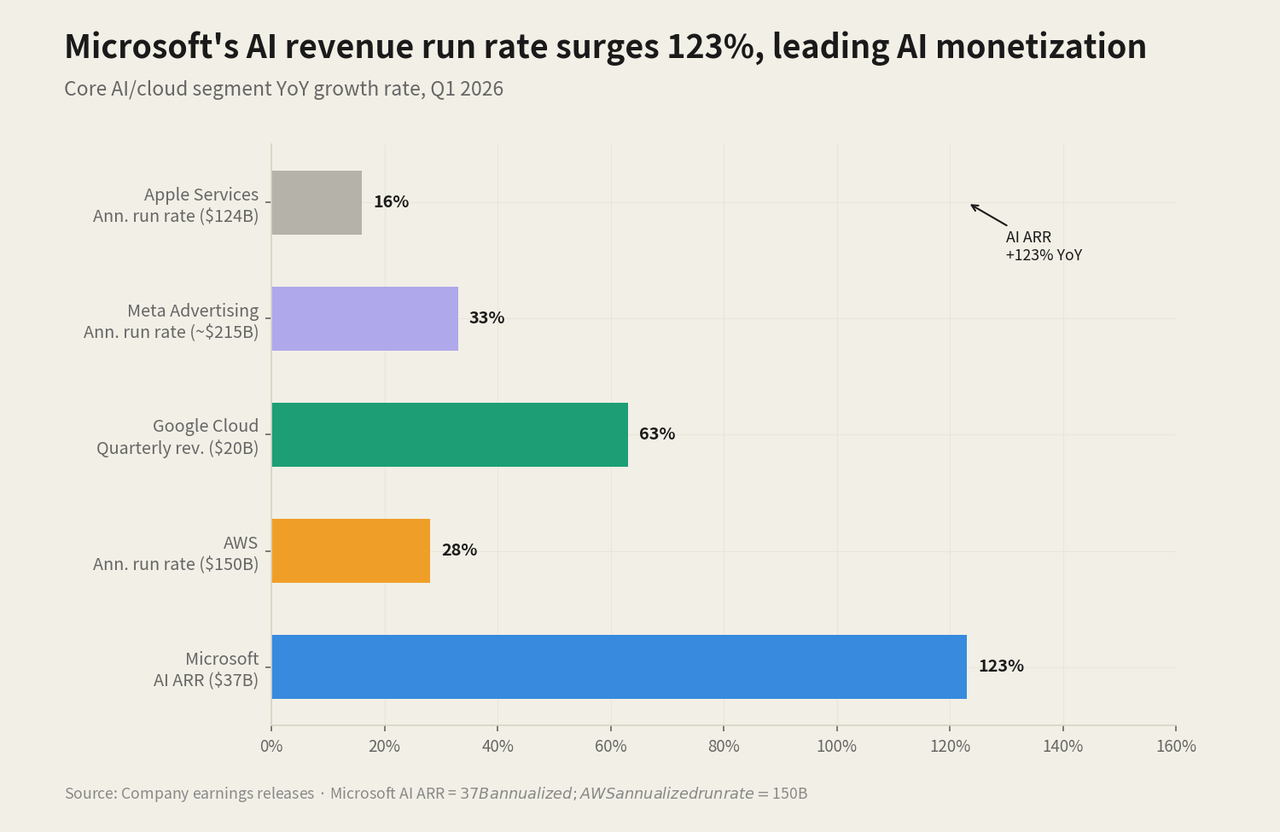

Microsoft leads the group in AI monetization, with its AI business reaching an annualized revenue run rate of $37 billion, a 123% increase year over year. This revenue includes Azure AI services, model builder revenue, and Microsoft’s proprietary AI tools such as Copilot. Satya Nadella summarized the quarter: “Cloud and AI are the essential inputs for every business to expand output, reduce costs, and accelerate growth.”

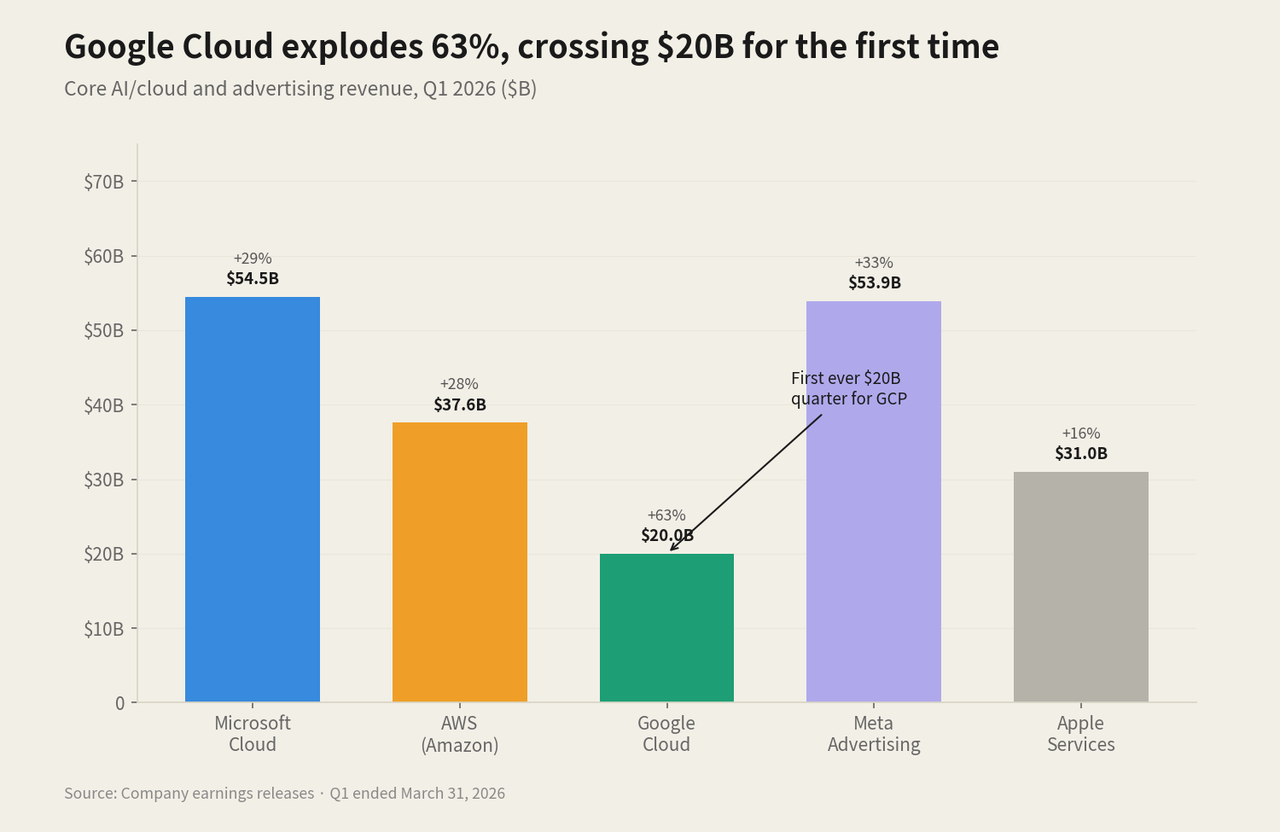

Azure and other cloud services grew 40% year over year. The Intelligent Cloud segment generated $34.68B. Microsoft 365 Copilot commercial paid seats surpassed 20 million. Azure OpenAI Service now counts more than 75,000 customers.

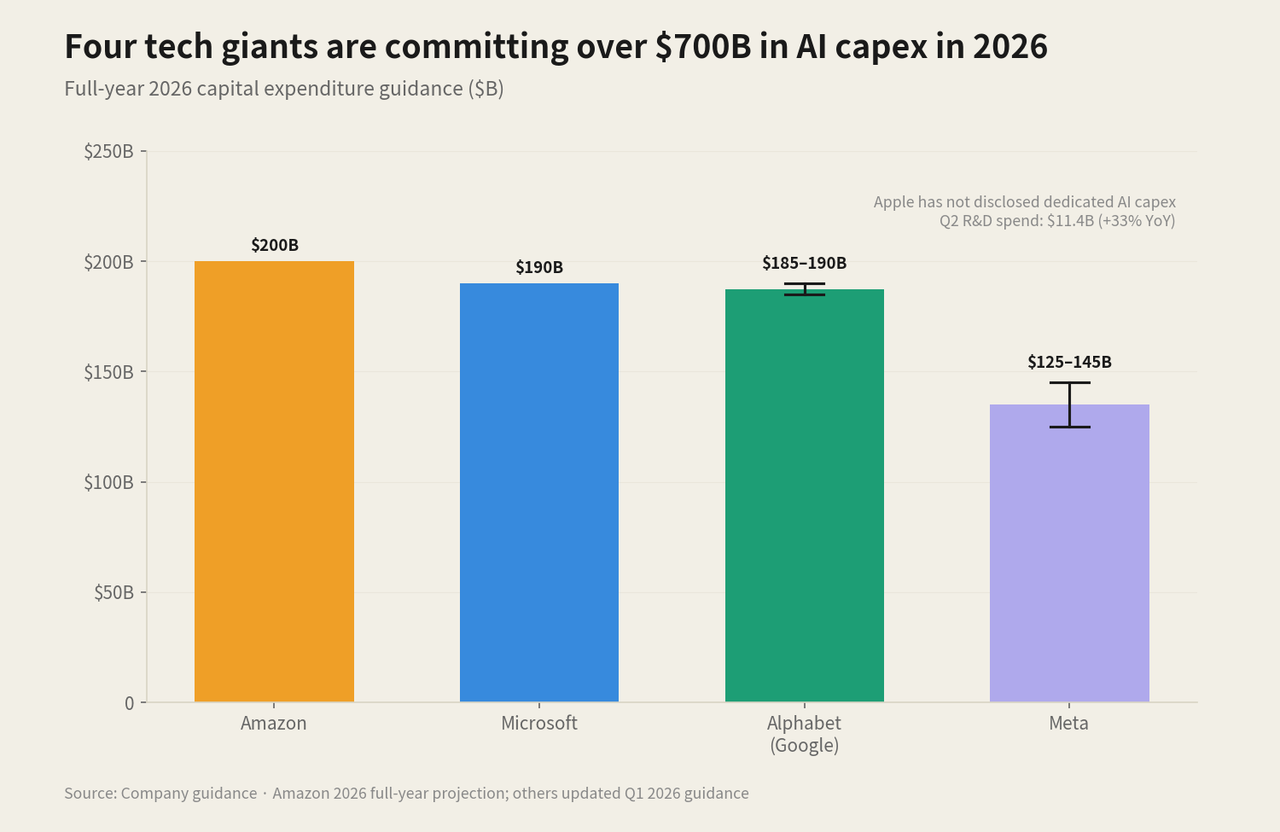

The capital commitments are equally significant. Q3 capex came in at $31.9B. Management guided Q4 capex above $40B and raised the full calendar year 2026 outlook to approximately $190B, roughly $25B of which is attributable to higher component pricing, particularly memory. Commercial remaining performance obligations reached $627B, up 99% year over year. That figure represents exceptional forward revenue visibility.

Of the five, Microsoft has the most direct line from AI investment to reported revenue. A $37B run rate growing at 123% means Copilot and Azure AI are no longer in the adoption phase. The current constraint is the compute supply, not the customer demand.

III. Alphabet: Cloud Accelerates, Search Holds Its Ground

Google Cloud generated $20.03B in quarterly revenue, up 63% year over year, well above the $18.05B Wall Street estimate and the first time Cloud has crossed $20B in a single quarter. The Cloud backlog nearly doubled quarter over quarter to more than $460B.

The AI monetization within Cloud is accelerating sharply. Revenue from products built on Google’s generative AI models grew nearly 800% year over year. Enterprise AI solutions became Google Cloud’s primary growth driver for the first time. The Gemini API is now processing more than 16 billion tokens per minute.

The persistent concern that AI search would cannibalize Google’s advertising business appears, for now, unfounded. Search and Other revenue grew 19% to $60.4B. YouTube advertising increased by 11% to $9.88B. AI Overviews reaches 1.5 billion monthly users. Gemini Enterprise paid monthly active users grew 40% quarter over quarter.

One detail from the earnings call deserves attention. Sundar Pichai acknowledged that Google Cloud is compute-constrained in the near term, and that revenue would have been higher had the company been able to fully meet demand. Alphabet raised its full-year 2026 capex guidance to as much as $190B.

Alphabet’s AI position is the most vertically integrated of the group, spanning chip design, model infrastructure, search, and enterprise cloud. The 63% Cloud growth rate was achieved while supply-constrained, making it the strongest single data point of the earnings week. Search, widely expected to be most at risk from AI disruption, is instead growing faster because of it.

IV. Amazon: AWS Posts Fastest Growth in 15 Quarters, Custom Chip Business Emerges

AWS revenue reached $37.59B in Q1, up 28% year over year, beating the $36.64B Wall Street consensus and representing the segment’s fastest growth in 15 quarters. AWS’s operating income grew roughly 23% to $14.16B, well above the $12.84B consensus.

The strategically significant development this quarter is Amazon’s homegrown chip business. Its custom silicon operation now carries an annualized revenue run rate above $20B, growing triple digits year over year. Trainium2 offers roughly 30% better price-performance than comparable GPUs and is largely sold out. Trainium3, which began shipping at the start of 2026, is nearly fully subscribed. Amazon Bedrock client spending grew 170% quarter over quarter, with Q1 alone processing more tokens than all prior years combined.

The ecosystem commitments this quarter extend that advantage further. Anthropic will secure up to 5 gigawatts of Trainium chips. OpenAI is committed to approximately 2GW of Trainium capacity through AWS infrastructure, with ramp-up beginning in 2027. Amazon’s Q1 capital expenditures reached $44.2B, with full-year 2026 capex projected at approximately $200B.

Amazon is expanding beyond cloud services. Securing both Anthropic and OpenAI as major Trainium customers in the same quarter establishes its custom silicon as the core infrastructure for two leading AI labs. This position is more difficult to challenge than any advantage based on cloud pricing.

V. Meta: Advertising and AI Dual Engine, $145B Capex Bet

Meta’s AI investments are producing measurable advertising results. Ad impressions grew 19% year over year, while average price per ad rose 12%. Both moving simultaneously reflects AI-driven improvements to targeting and delivery, compounding returns within the existing business.

On the model front, Meta announced the release of its first foundation model from Meta Superintelligence Labs, with Muse Spark as the flagship product. Family daily active people reached 3.56 billion in March 2026, up 4% year over year.

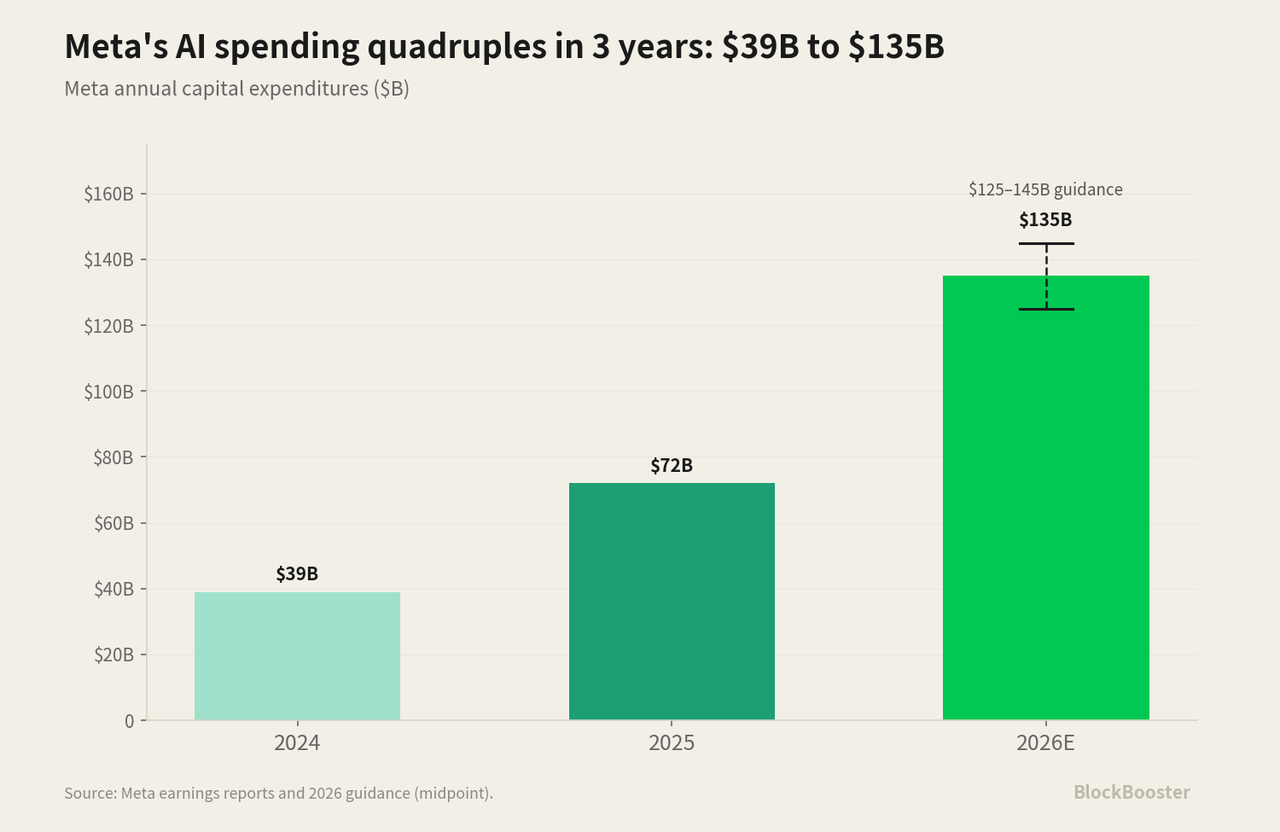

Capital expenditure is where the market pushed back. Meta raised its full-year 2026 capex guidance to $125B to $145B, up from the prior range of $115B to $135B, citing higher component pricing and additional data center costs. Despite a significant earnings beat, the stock fell as much as 10% in early trading as investors weighed when the spending would translate into revenue streams beyond advertising.

Meta’s AI returns today are real but indirect: the same advertising business, running more efficiently. Muse Spark represents a bet on owning the model layer, but there is no clear near-term revenue line attached to it. Of the five companies, Meta carries the widest gap between current AI spend and demonstrable AI revenue.

VI. Apple: The Quietest AI Play, R&D Up 33%

Apple’s AI narrative has been comparatively understated relative to the other four. The numbers suggest a different posture. R&D spending jumped to $11.42B in the quarter, up 33% year over year, far outpacing the company’s 17% revenue growth. Tim Cook explicitly cited AI as a key driver, noting Apple is “clearly investing more.”

On the earnings call, Apple positioned the Mac mini and Mac Studio as premier platforms for AI and agentic tools, noting customer recognition of this capability is happening faster than the company anticipated, driving higher-than-expected demand for both products. Apple signaled significant AI announcements at the upcoming WWDC and attributed strong MacBook Neo demand in part to on-device AI capabilities.

Apple authorized an additional $100B share repurchase program and guided next-quarter revenue growth of 14% to 17%, well above the 9.5% analysts had expected.

Apple’s strategy does not produce a labeled AI revenue line today. What it produces is a hardware differentiation argument: on-device inference as a primary purchase reason for iPhone and Mac, compounding through Apple Silicon. The R&D acceleration suggests the commercial payoff is being built, not deferred.

VII. Three Cross-Cutting Themes

Theme 1: Cloud is the most direct AI monetization channel

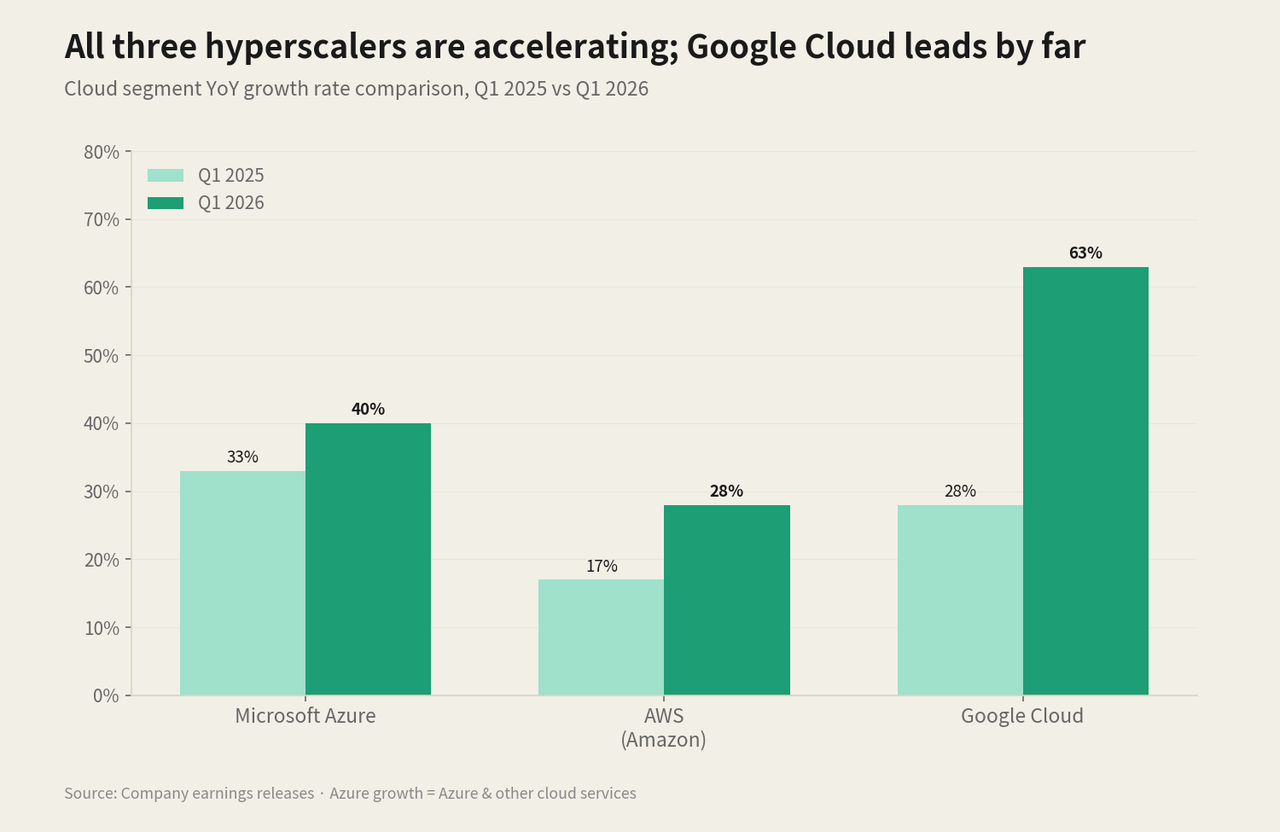

All three hyperscale cloud platforms accelerated this quarter — Azure to 40%, AWS to 28%, Google Cloud to 63%. All three companies acknowledged being supply-constrained: demand is outpacing the ability to deploy compute. This is a high-quality problem and a meaningful signal — it suggests AI cloud demand is real and currently being suppressed, not inflated.

Theme 2: The capex race has entered uncharted territory

The four major AI infrastructure investors — Amazon, Microsoft, Alphabet, and Meta — are collectively guiding to more than $700B in capital expenditure for 2026 alone. Amazon projects $200B; Microsoft approximately $190B; Alphabet up to $190B; Meta $125B–$145B. The direct beneficiaries of this spending are semiconductor companies (Nvidia, AMD, and increasingly Amazon’s own Trainium), data center construction firms, and power infrastructure providers.

Theme 3: AI monetization is stratifying clearly

The five companies represent five distinct positions on the AI monetization spectrum:

-

Clearest ARR (quantified AI revenue): Microsoft ($37B ARR, +123%)

-

Infrastructure-driven: Amazon (AWS + Trainium), Alphabet (Cloud + Gemini)

-

Efficiency-driven: Meta (AI improves ad systems)

-

Hardware/ecosystem-driven: Apple (Apple Silicon + Apple Intelligence + Services)

Closing Thought

The Q1 2026 earnings cycle delivered a clear verdict. AI is not a story about future potential. It is a present-day force actively reshaping cloud, advertising, search, and silicon. The combined AI-related capex commitments of these five companies are large enough to redefine the scale of the entire semiconductor and data center industry.

The question worth asking now is no longer whether AI can be monetized. It is which of these companies can convert infrastructure investment into durable, high-margin returns, and how fast.